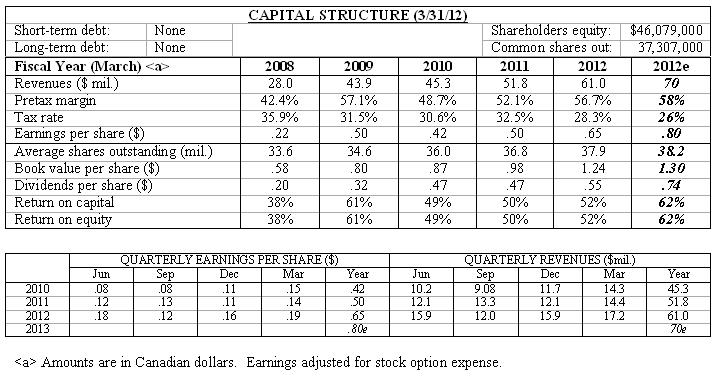

3-S Bio (SSRX $13.25) reported excellent on target Q1 results. Sales climbed 24% to $23.4 million. Earnings surged 53% to $.23 a share. Selling prices were generally unchanged compared to the December period, although they did decline 3%-5% from the year ago quarter. Volume remained robust despite the fact prices probably will be forced lower by new Government regulations. Those have not be formalized yet but are expected to go into effect in Q2. In theory, customers could have waited for the prices to fall before purchasing in Q1. China established its own health reform law in 2010, expanding coverage to most of the country. The quid pro quo with the health care community has been one of greater volume in exchange for lower prices. The upcoming round could see 3-S Bio impacted by 5%-10%.

Margins held up well after prices were reduced last year. 3-S Bio built a series of new manufacturing facilities which came on stream in 2011. Modernized equipment and procedures enabled the company to cut production costs directly. Depreciation expense jumped in the short run, though, since the new facilities were 4x larger than the former site. The company now has ramped up volume sufficiently to achieve 50% capacity utilization rates. Further cost reductions are possible, suggesting overall margins will remain attractive despite the Government's upcoming price cuts.

Marketing efforts are accelerating. 3-S Bio plans to boost its distribution channel by 20%-25% this year, with an emphasis on penetrating second tier hospitals. Those customers are exhibiting the fastest growth as the health law kicks in. The company also recently formed a joint venture with U.S. based Davita to set up a chain of dialysis centers in two Chinese provinces. That deal is likely to begin contributing early next year. New products are in the pipeline, moreover. And export operations are picking up momentum. A new version of the company's top selling drug will enter clinical trials this year. Other trials are approaching the finish line. Those include products licensed from international companies for sale in China. 3-S Bio's new facilities also are being fine tuned to make generic biological drugs. Those are off patent biotech products that offer huge potential but even western companies find challenging to make. Exports remain focused at high population mid range countries like Egypt and Turkey which need high quality products at affordable prices.

Our estimates are unchanged. A stronger performance is possible if the next round of Government price reductions come in at the low end of the anticipated range. The long term outlook remains bright. 3-S Bio is well positioned to expand in China without government help. Its world class scientific talent promises to attract additional foreign partnerships. Finances are solid. And for a bunch of scientists, the management has a proven track record when it comes to marketing pharmaceuticals.

( Click on Table to Enlarge )